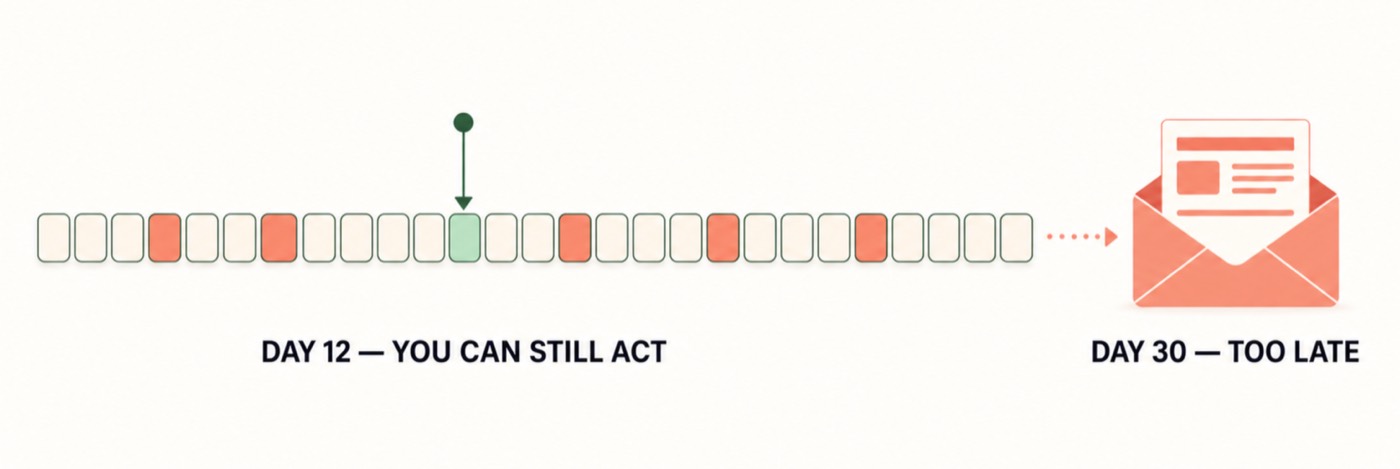

Budgets are not a bad idea. They are a late idea. You pick €400 for eating out in January, and on the 3rd of February your app tells you the answer was €517. You now know something true, actionable in no way whatsoever, about a month that has ended.

Nothing about that number is wrong. The problem is that it arrived after the last chance to change it.

Feedback works when it is close to the action

There is a well-studied reason spending feels frictionless in a way that saving does not. Prelec and Loewenstein called it the pain of paying: the discomfort of parting with money is strongest when payment and consumption are close together, and it fades as they are pulled apart.1 Cash hurts. Card hurts less. Tap-to-pay hurts least of all, because by the time the statement arrives, the coffee is a memory and the €4.20 is a line item among two hundred others.

A budget is feedback delayed by up to 31 days. Almost nothing else in your life gets corrected on a 31-day loop.

Consider how you actually manage things that work: you do not weigh yourself once a month and then reason about January. You do not check the fuel gauge on the last day of the trip. The loop is short, the signal is ambient, and the correction is small and continuous.

What a day tells you that a month cannot

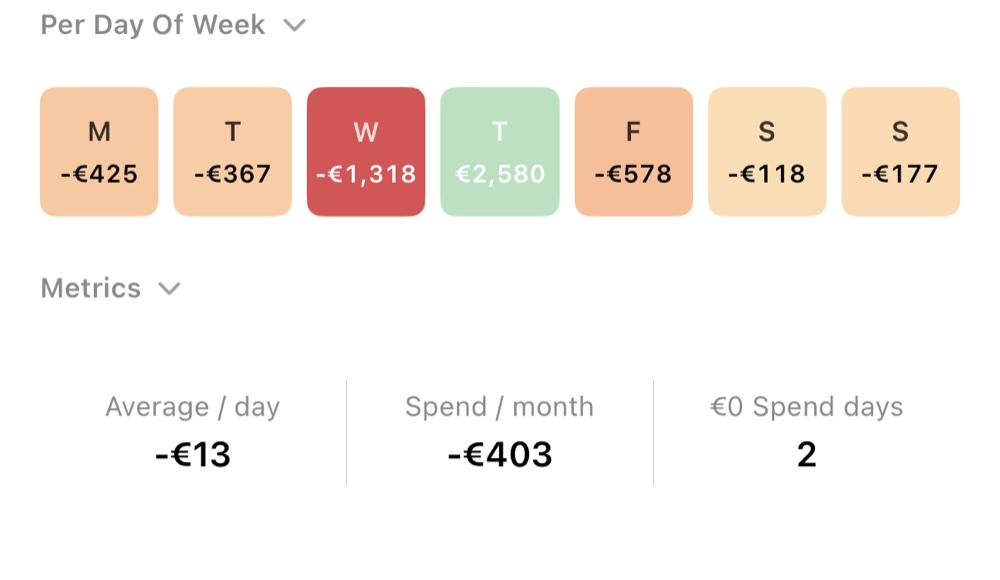

A monthly total is one number describing thirty different days. It collapses everything that would have told you what to do:

- Shape. €1,200 spread evenly is a life. €1,200 concentrated in six days is a habit, and habits have a trigger.

- Rhythm. If four of your five heaviest days are Saturdays, that is not a budgeting problem. It is a Saturday problem, and it has a solution.

- Drift. Two months at €1,200 can hide a category quietly doubling while another halves. The total says nothing changed.

- The obvious outlier. One €340 day usually explains a “bad month” entirely. Once you see it, there is often nothing else to fix.

Awareness is not the same as restriction

This is the part that gets missed. Daily awareness is not a stricter budget. It has no limit, no category caps, nothing to fail at. You are not being told no. You are being told what is happening, early enough that the response is a small adjustment rather than a resolution.

Practically, on the 12th of a heavy month you have eighteen days of ordinary decisions left. Each one is easy. On the 3rd of the following month you have zero, and the only tool left is guilt, which has never once reduced anyone’s grocery bill.

How to do this without an app

You genuinely do not need software. The mechanism is what matters, and the mechanism is: look at the days, not the month, while the month is still running.

- Once a week, glance at the last seven days rather than the running total.

- Ask one question: which day was the heaviest, and why?

- Do not set a target. Just notice. Noticing is most of the effect.

Pocket Pivot exists because doing that by hand across several banks is tedious enough that people stop. A calendar of coloured days does the noticing for you: a heavy week is a patch of red you see in half a second, without reading a single number.

The one thing worth remembering

Budgets answer did I overspend?, a question that can only be answered too late. Daily patterns answer am I overspending?, which is a question you can still do something about.

Sources

- Drazen Prelec & George Loewenstein, “The Red and the Black: Mental Accounting of Savings and Debt”, Marketing Science 17(1), 1998. doi.org/10.1287/mksc.17.1.4

Notice the pattern while you can still change it

Pocket Pivot colours every day by what you spent, across every bank you connect.

Stay informed about early accessPocket Pivot is a spending-awareness tool. Nothing here is financial, investment, tax or legal advice.